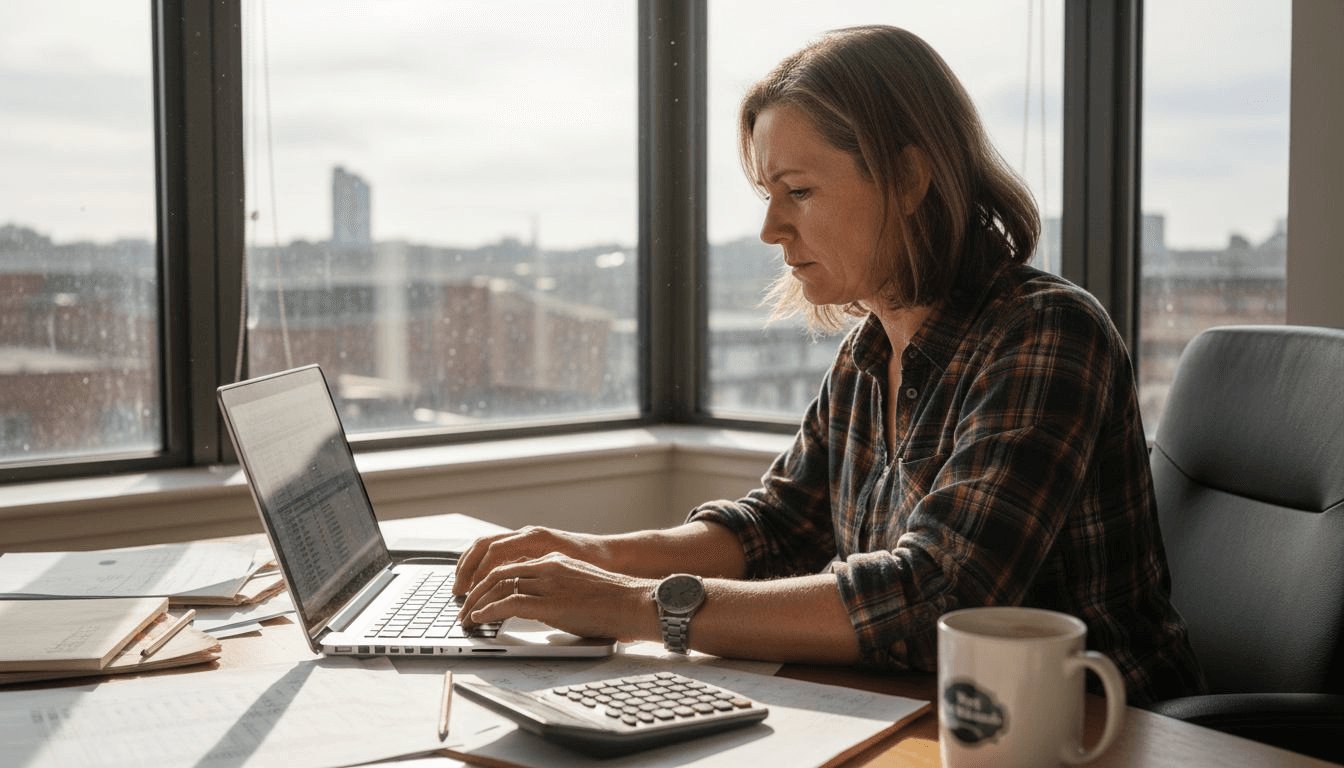

Running a small or medium-sized business in Birmingham means juggling countless financial tasks every day. Missing a single transaction or delaying an invoice can quickly lead to confusion, lost revenue, or even costly penalties. Keeping your records in order often feels overwhelming, especially with so many details to monitor and deadlines to meet.

The right bookkeeping habits can turn this chaos into clarity. Practical steps—like recording daily transactions, managing accounts receivable and payable, and reconciling your bank statements—offer clear answers and peace of mind. Each adjustment you make brings more control over your cash flow and helps you avoid avoidable mistakes.

Discover effective, straightforward methods proven to improve accuracy, support compliance, and protect your business relationships. The next set of insights reveal approaches you can start using straight away, giving you confidence in your financial management and a stronger foundation for success.

Table of Contents

- 1. Recording Daily Transactions for Accuracy

- 2. Managing Accounts Receivable Efficiently

- 3. Tracking Accounts Payable to Avoid Late Fees

- 4. Reconciling Bank Statements Regularly

- 5. Processing Payroll and Employee Expenses

- 6. Preparing Financial Reports for Compliance

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Record Transactions Daily | Consistent daily logging prevents accounting errors and ensures details are fresh, increasing accuracy in financial management. |

| 2. Manage Accounts Receivable Proactively | Track unpaid invoices and follow up regularly to improve cash flow and reduce collection challenges. |

| 3. Organise Accounts Payable Systems | Implement a structured process for tracking invoices to avoid late payments and enhance supplier relationships. |

| 4. Regularly Reconcile Bank Statements | Monthly reconciliation helps detect discrepancies early, preventing potential financial issues and ensuring accurate records. |

| 5. Prepare Financial Reports Frequently | Regular financial reporting captures performance and supports compliance, allowing timely adjustments based on accurate data. |

1. Recording Daily Transactions for Accuracy

Daily transaction recording forms the foundation of reliable financial management for SMEs. Without consistent daily entries, small discrepancies compound into significant accounting errors that threaten compliance and decision-making.

When you record transactions daily, you capture business events whilst they're fresh and details are clear. This immediate recording prevents the common mistake of trying to reconstruct events weeks later from scattered receipts and incomplete notes.

According to IRS guidance on how to record business transactions, a solid system requires daily entries in journals and ledgers. Whether you use electronic software like Xero or Sage, or maintain paper records, consistency matters more than the medium.

What Daily Transaction Recording Actually Involves

Daily recording follows a specific process that ensures accuracy at each stage:

- Analysing the transaction: Identify what happened (sale, expense, bank deposit) and classify it correctly

- Entering into journals: Record the transaction with proper debit and credit entries following accounting rules

- Posting to ledgers: Transfer the journal entry to the appropriate account ledger for tracking

- Verifying accuracy: Cross-check amounts and classifications before filing

Daily recording ensures transactions are captured timely, preventing errors and discrepancies that become costly to correct later.

Your team should record cheque book entries, cash receipt summaries, and compensation records on the same day transactions occur. This daily discipline becomes routine once established and protects your financial records from gaps and omissions.

For Birmingham SMEs managing multiple transactions, setting a specific time each afternoon (say 3pm) for recording prevents backlogs. Even 15 minutes daily beats four hours of scrambling on Friday afternoon.

The stakes matter here. Tax authorities expect accurate records. Lenders scrutinise clean transaction histories. Your own decision-making depends on knowing what actually happened financially.

Pro tip: Dedicate the same time each working day to transaction entry, so recording becomes automatic rather than a task you forget until month-end.

2. Managing Accounts Receivable Efficiently

Accounts receivable management is where money you've earned actually becomes money in your bank account. Without proper systems, invoices slip through the cracks and cash flow suffers.

For Birmingham SMEs, accounts receivable represents real working capital tied up in unpaid invoices. The longer money stays outstanding, the harder it becomes to pay your own suppliers and staff on time.

Effective AR management involves three core activities that work together. You must track who owes you money, monitor how long they've owed it, and pursue collection professionally. This isn't aggressive. It's protecting your business.

The Mechanics of Proper AR Management

Proper accounts receivable management includes recording receivables after documentation, maintaining subsidiary ledgers, and regular statement generation. You need systems that show exactly who owes what and when payment is due.

Key activities you should implement:

- Recording receivables: Document each sale with a clear invoice showing amount, terms, and due date

- Maintaining subsidiary ledgers: Keep detailed records of each customer's balance and payment history

- Generating ageing reports: Review outstanding invoices by how long they've been unpaid (30, 60, 90+ days)

- Following up on overdue accounts: Contact customers systematically before invoices reach 60 days outstanding

- Resolving disputes: Address customer complaints quickly so payment delays don't stem from misunderstandings

Proper AR management improves cash flow, mitigates credit risks, and supports accurate financial reporting.

Technology makes this manageable. Software like Xero or Sage automatically tracks invoices, sends payment reminders, and generates ageing reports showing exactly which accounts need attention.

Consider implementing clear payment terms upfront. Stating "Payment due within 14 days" creates expectation and gives you grounds to follow up on day 15.

Your team should also establish who's responsible for collections. Whether that's your finance manager or bookkeeper, one person owning the process prevents invoices from being forgotten.

Pro tip: Set up automatic payment reminders one week before the due date, then follow up with phone calls or emails on day one past due, before accounts age further.

3. Tracking Accounts Payable to Avoid Late Fees

Late payments to suppliers damage relationships and drain money through unnecessary fees. Yet many SMEs struggle with accounts payable simply because invoices arrive haphazardly and due dates get lost.

Accounts payable management means knowing exactly what you owe, to whom, and when payment is due. It's the counterpart to accounts receivable, but this time you're the one being chased for payment.

Late fees might seem small per invoice. But a 2% penalty on a £5,000 supplier invoice costs £100. Miss ten invoices annually and you've wasted £1,000 on entirely preventable charges. That money could hire part-time help or fund business growth.

Beyond fees, late payments erode vendor relationships. Suppliers remember unreliable payers. When supply shortages occur, they prioritise customers who pay on time. You could face delayed shipments or higher pricing because of poor payment history.

Building Your Accounts Payable System

Efficient AP tracking requires organized workflows and regular oversight to prevent errors and ensure timely payments. You need a process that catches invoices before they become late.

Your AP system should include:

- Invoice capture: Record every supplier invoice immediately upon receipt, not when you remember

- Due date tracking: Enter payment due dates clearly so nothing gets missed

- Payment schedule: List all invoices by due date so you see cash outflows coming

- Segregation of duties: Have someone verify invoices before someone else pays them

- Regular review: Check your accounts payable balance weekly to spot discrepancies

Robust internal controls and automation streamline accounts payable, ensuring payments are accurate and on time.

Many SMEs use spreadsheets for this, which works if discipline is maintained. Software like Xero or Sage automates much of this work, sending alerts before due dates arrive and preventing duplicate payments.

Small details matter. If a supplier's standard terms are Net 30, paying on day 31 damages your reputation. Build in a two-day buffer so you always pay slightly early. It costs nothing and strengthens relationships.

Pro tip: Schedule a weekly 20-minute AP review every Monday morning to process invoices and plan the week's payments, preventing last-minute scrambling.

4. Reconciling Bank Statements Regularly

Bank reconciliation is where your internal records meet reality. Your bookkeeping might show £10,500 in the account, but the bank says £10,200. Without reconciliation, you won't know which figure is correct or why they differ.

Bank reconciliation means comparing your accounting records against the bank statement to find discrepancies. It sounds tedious, but it's one of the most powerful fraud prevention and error-detection tools you have.

Think of it this way. Cheques you've written take time to clear. Deposits you've recorded might not have hit the bank yet. Bank charges appear on statements but might not be in your books. These timing differences are normal. But a £2,000 withdrawal you never authorised is not normal, and reconciliation catches it.

For Birmingham SMEs, monthly reconciliation is standard practice. You should complete it within days of receiving your statement, whilst transactions are fresh and easy to trace.

How Bank Reconciliation Works

Monthly bank reconciliations match your accounting ledger with bank statements to verify deposits, withdrawals, charges, and interest. The process identifies timing differences and errors that must be corrected.

Your reconciliation checks for:

- Outstanding cheques: Cheques you've written but haven't cleared the bank yet

- Deposits in transit: Money you've recorded but the bank hasn't received yet

- Service charges: Bank fees that appear on statements but weren't in your records

- Interest earned: Interest credited by the bank

- Errors: Transposition mistakes or duplicate entries in either system

Regular reconciliation helps detect errors, prevent fraud, and ensure the accuracy of financial data.

Start by listing all outstanding cheques and deposits in transit. Then adjust your book balance to match the bank statement. Once they agree, you're done. If they don't match, the difference is usually small and traceable.

Keeping your records current makes this easier. If you record transactions daily (as discussed in item 1), reconciliation takes minutes rather than hours.

Many SMEs discover errors during reconciliation that would have caused serious problems later. A missing invoice, a duplicate payment, or an unauthorised charge gets caught before it becomes costly.

Pro tip: Reconcile immediately after receiving your statement, whilst you can still reach the bank to dispute charges or investigate discrepancies.

5. Processing Payroll and Employee Expenses

Payroll is often the largest expense for SMEs, and it's also one of the most heavily regulated. Calculate wages incorrectly or miss a tax deadline, and you face penalties that sting.

Payroll processing involves calculating wages, withholding taxes, handling deductions, and ensuring timely payments to employees. It requires accuracy because mistakes affect both your finances and your employees' take-home pay.

Many business owners underestimate payroll complexity. It's not just dividing annual salary by 12. You must account for National Insurance contributions, income tax withholding, pension contributions, and benefits. Different employees have different circumstances. And tax rules change annually.

Beyond wages, employee expenses like mileage, training costs, or equipment reimbursements must be tracked and processed correctly. Poor expense handling creates confusion, reduces employee trust, and complicates your accounts.

Building a Payroll System That Works

Standard operating procedures for payroll help SMEs streamline processing steps from time approval through to timely payment. Clear SOPs set roles, safeguard data, and ensure tax compliance.

Your payroll system should include:

- Time tracking: Capture hours worked accurately, whether via timesheets or software

- Wage calculation: Apply correct rates, overtime rules, and allowances consistently

- Tax withholding: Deduct correct PAYE and National Insurance amounts

- Pension contributions: Handle workplace pension schemes properly

- Expense documentation: Record and approve employee expenses with receipts

- Payment processing: Transfer wages on schedule, every single month

- Compliance records: Keep documentation for tax authorities and audits

Proper payroll processing ensures legal compliance, financial accuracy, and employee satisfaction.

For small teams, payroll software like Sage Payroll or specialist providers handle calculations and tax compliance automatically. This reduces errors and saves your bookkeeper hours of manual work.

Whoever processes payroll should understand the legal requirements. Mistakes are expensive. HMRC penalties for late payments or incorrect reporting can quickly exceed £1,000. More importantly, underpaying tax withholding creates liability that the business must cover.

Employee morale depends on accurate, timely payments. Even one late payslip creates frustration and questions about whether you can be trusted. Consistency matters enormously.

Pro tip: Process payroll on the same date each month before the payment deadline, then verify amounts match timesheets before processing, preventing errors that are painful to correct.

6. Preparing Financial Reports for Compliance

Financial reports are where all your bookkeeping work comes together. They tell you whether your business is profitable, show lenders and investors your financial health, and satisfy regulatory requirements.

Without proper financial reports, you're flying blind. You don't know if you're actually making money. Tax authorities won't accept vague estimates. Banks won't lend based on hunches. Your reports must be accurate, complete, and prepared according to recognised standards.

For Birmingham SMEs, financial reporting requirements depend on your business structure and size. But regardless of specifics, the principle is the same. Your reports must reflect the true financial position of your business.

Proper financial reporting starts with proper bookkeeping. If your daily transactions are recorded accurately, bank accounts reconciled, and invoices tracked, preparing reports becomes straightforward. If your books are messy, reports become guesswork.

What Financial Reports Include

Maintaining accurate records helps prepare financial statements that comply with generally accepted accounting principles. Three core reports form the foundation of financial reporting.

Your essential financial reports are:

- Balance sheet: Shows what you own (assets), what you owe (liabilities), and your equity on a specific date

- Profit and loss statement: Shows income, expenses, and whether you made a profit or loss over a period

- Cash flow statement: Shows actual money moving in and out, revealing whether you have enough cash to operate

These three reports paint a complete picture. The balance sheet shows your financial position. The profit and loss shows profitability. The cash flow shows liquidity. Together, they tell stakeholders everything they need to know.

Accurate bookkeeping and proper accounting methods ensure financial statements comply with recognised standards and support informed decisions.

For SMEs, IFRS for SMEs provides a simplified framework that reduces complexity whilst ensuring compliance. You don't need full IFRS complexity. The SME standard strikes the right balance.

Most bookkeeping software generates these reports automatically. Enter transactions correctly, and your software calculates figures and produces formatted reports ready for tax filing or stakeholder review.

Regulatory bodies expect reports prepared consistently. If you change how you measure inventory or depreciate assets, you must disclose the change. Consistency builds credibility.

Pro tip: Prepare draft financial reports quarterly rather than waiting until year-end, so you catch errors early and understand your financial performance throughout the year.

Below is a comprehensive table summarising the strategies and principles covered throughout the article regarding financial management for Birmingham SMEs.

| Topic | Key Insights | Implementation Actions | Advantages |

|---|---|---|---|

| Recording Daily Transactions | Establishes accuracy and prevents errors by maintaining up-to-date financial records daily. | Schedule consistent daily transaction entry time. Use reliable recording software or methods. | Avoids inaccuracies, ensures compliance, and supports timely decision-making. |

| Accounts Receivable Management | Streamlines invoice tracking and collection processes to enhance cash flow. | Generate ageing reports, and set firm yet courteous collection practices. Use automated invoicing systems. | Reduces outstanding payments and maintains healthy cash flow. |

| Accounts Payable Tracking | Prevents overdue payments and unnecessary fees by systematically managing supplier invoices. | Record invoices upon receipt. Monitor due dates with software alerts or scheduling. | Enhances vendor relationships and avoids late fees. |

| Bank Reconciliation | Matches internal records with bank statements for accuracy verification. | Perform monthly reconciliations promptly. Investigate discrepancies immediately. | Prevents fraud and highlights financial reporting errors. |

| Payroll Management | Processes employee compensation accurately, adhering to legal standards. | Use payroll software to calculate wages and ensure compliance with regulations. Collect and document all expense claims. | Guarantees timely payments, retains employee trust, and achieves compliance. |

| Financial Reporting | Combines all bookkeeping into reports needed for insights and regulatory compliance. | Produce periodic reports for stakeholders using standardised accounting frameworks. | Provides accurate business performance insights and ensures compliance. |

Strengthen Your SME’s Accounting with Expert Bookkeeping Talent

Managing essential bookkeeping tasks such as daily transaction recording, accounts receivable and payable, payroll, and bank reconciliations can strain small businesses in Birmingham. These fundamental activities require precision and efficiency to avoid costly errors, late fees, and cash flow issues. When your team struggles with the volume or complexity of these duties, your financial clarity and compliance are at risk.

At Ibaco Recruitment, we understand these challenges deeply. With our local knowledge of Birmingham and West Midlands markets plus expertise in accounting standards and software like Xero and Sage, we connect your business with thoroughly vetted finance professionals ready to take ownership of these critical bookkeeping functions. Whether you need a skilled bookkeeper familiar with daily transaction management or someone who can streamline payroll processing and compliance, our recruitment process ensures fast placements with no upfront fees.

Don’t let bookkeeping errors or time-consuming processes hold your SME back. Visit Ibaco Recruitment today and submit your hiring request. Get matched quickly with qualified candidates who will keep your finances accurate and on track so you can focus on growing your business.

Frequently Asked Questions

What are the key bookkeeping tasks that SMEs should perform daily?

Daily bookkeeping tasks for SMEs include recording transactions, monitoring accounts receivable, and managing accounts payable. To maintain accuracy, ensure you enter all transactions consistently at the end of each business day.

How can I improve my accounts receivable management?

Improving accounts receivable management involves tracking outstanding invoices and setting clear payment terms for customers. Follow up on overdue accounts systematically to collect payments within 30 days to maintain healthy cash flow.

Why is regular bank reconciliation important for SMEs?

Regular bank reconciliation is crucial because it helps identify discrepancies between your records and the bank's statements. Perform reconciliation monthly to catch errors early and ensure your financial data is accurate, preventing potential issues later.

What should be included in my financial reports as an SME?

Your financial reports should include a balance sheet, a profit and loss statement, and a cash flow statement. Prepare these reports quarterly to keep track of your financial health and understand your business performance throughout the year.

How can I effectively manage payroll and employee expenses?

To manage payroll and employee expenses effectively, implement a streamlined system for tracking hours worked and ensuring accurate tax withholdings. Review and process payroll monthly to ensure timely payments and prevent costly penalties.

Recommended

- Hire a Bookkeeper in Birmingham (2026 Guide) | IBACO Recruitment

- Hire Accountants in Birmingham (2026 Guide) | IBACO Recruitment Experts

- Finance Recruitment Trends in Birmingham (2026) | IBACO Recruitment

- Ibaco Recruitment | Bookkeepers & Accountants in Birmingham

- Role of Bookkeeping in Business Success for SMEs